Read article

MPR have developed EIGHT products, each specifically designed to match the requirements of a particular type of organisation.

MPR sets the highest standards. The CII is clear about the levels that need to be maintained to be Chartered and MPR is proud to be so.

Hidden in the depths of most Directors and Officers Liability (“D&O”) policies is a clause granting cover for Outside Directorship Liability (“ODL”).

In 2017, Tim Jones wrote an article titled Cyber events and the importance of incident response. A lot has happened since, so it seemed like an appropriate time to sense check the different approaches to underwriting Cyber Insurance that have developed.

Cyber Insurance remains a hot topic into 2024. With changing market conditions and increased competition, it can be difficult to keep up – especially when coupled with wider issues of the volatile threat landscape and systemic event concerns.

Directors and Officers Liability (“D&O”) policies (or D&O sections of Management Liability (“ML”) policies) do not usually exclude cover for employment claims. However, such cover is only of minimal use and is rarely triggered in disputes between employees and employers.

As with 2023, Management Liability (“ML”) claims continue to arrive from a variety of sources.

A picture of MPR.

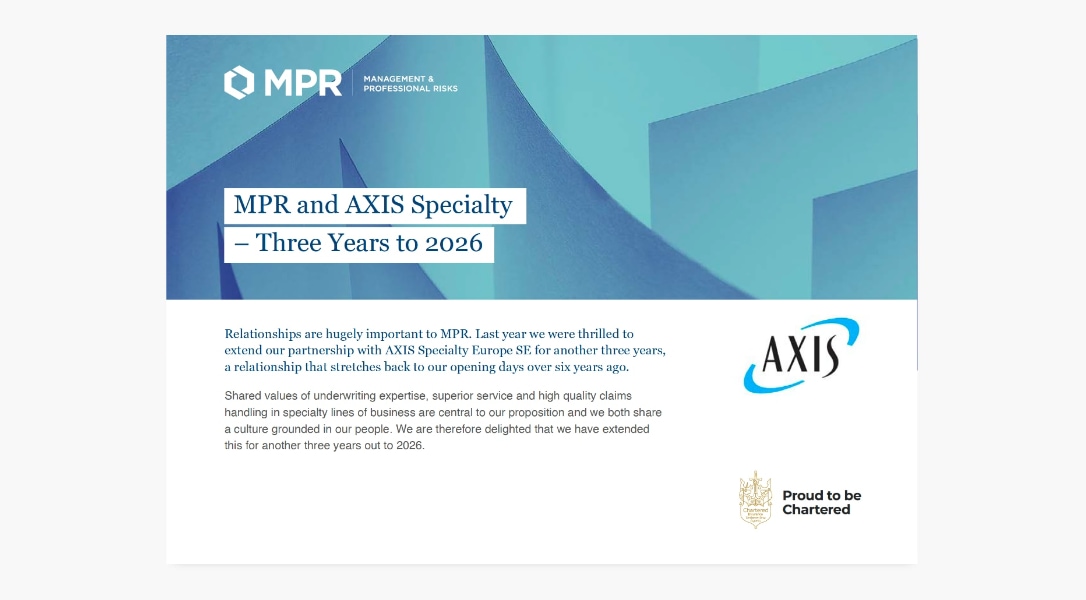

Relationships are hugely important to MPR. Last year we were thrilled to extend our partnership with AXIS Specialty Europe SE for another three years, a relationship that stretches back to our opening days over six years ago.

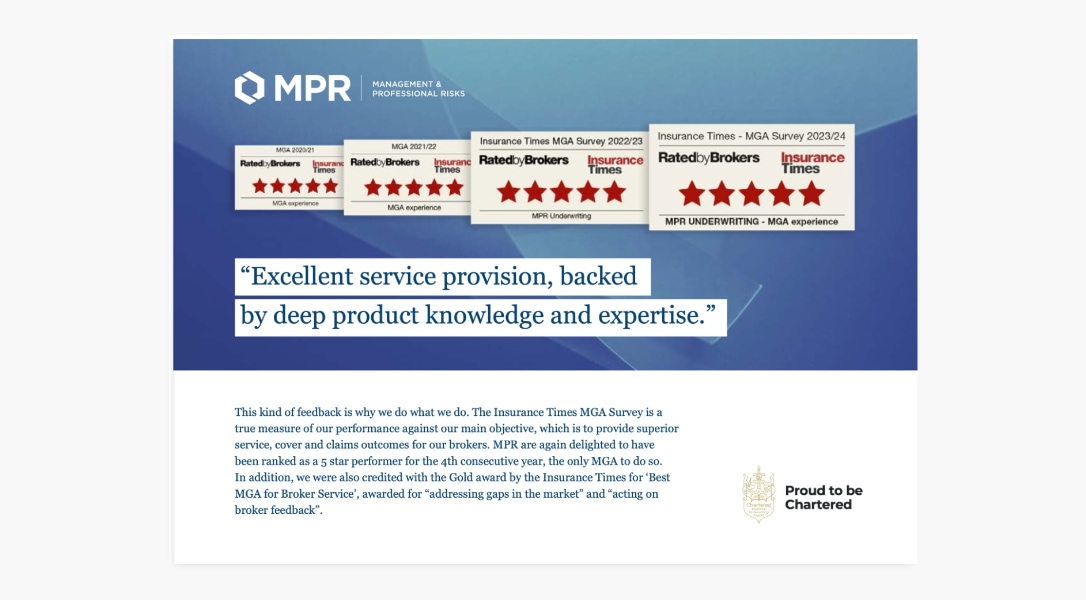

This kind of feedback is why we do what we do. The Insurance Times MGA Survey is a true measure of our performance against our main objective, which is to provide superior service, cover and claims outcomes for our brokers.

As UK brokers respond to this year’s MGA Survey, Insurance Times spoke to the Managing Director of MPR Underwriting, Neil McCarthy, about the challenges MGAs currently face and what considerations they need to keep an eye on moving forward.

When considering what limits to choose under a Management Liability (“ML”) policy, much of the focus centres on the Directors and Officers (“D&O”) liability section. Much less attention is given to the Employment Practices Liability (“EPL”) section, despite the fact that most ML professionals will attest to this being the more frequently notified section of the policy.

It is more than 15 years since The Corporate Manslaughter and Corporate Homicide Act 2007 (the “Act”) was introduced on 6 April 2008. The Act was an attempt to make it easier for the authorities to prosecute organisations where a corporate management failing caused a fatality.

External fraud in the UK is on the rise and, whilst accounting fraud has reduced since the last report, it is likely that alternative working practices necessitated by Covid means that some frauds are yet to be discovered.

The cyber market has seen some recent instability. A wave of cyber events (particularly Ransomware) drove harder market conditions and the raising of the bar on cyber security requirements. This has attracted new insurers and competition is intensifying again.

It is abundantly clear that not all Management Liability (“ML”) policy wordings are of the same quality. The difference is perhaps more acutely observed when comparing off line language with e-traded/statement of fact based policies.

MPR has now been established for over 6 years and since then we have observed many Management Liability claims. Perhaps as might be expected, there is a noticeable increase in regulator activity during that period.

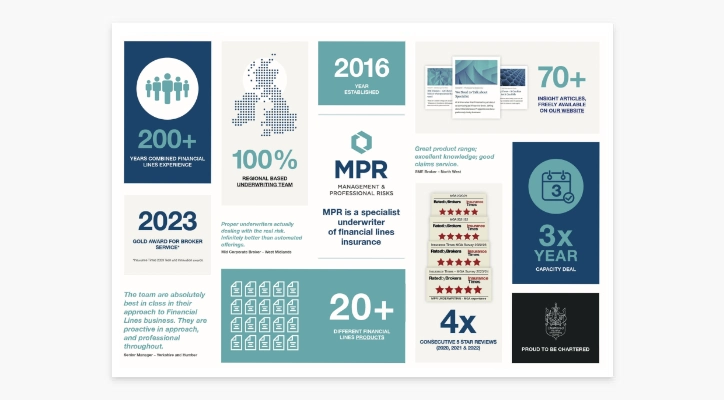

Since MPR was established in 2016, we have gone from strength to strength.

The construction of an exclusion is vital to its operation and impact. The preamble can often be more fundamental to the outcome than the language that follows.

We are delighted to have been ranked the overall best performing MGA in the Insurance Times Broker MGA survey 2022.

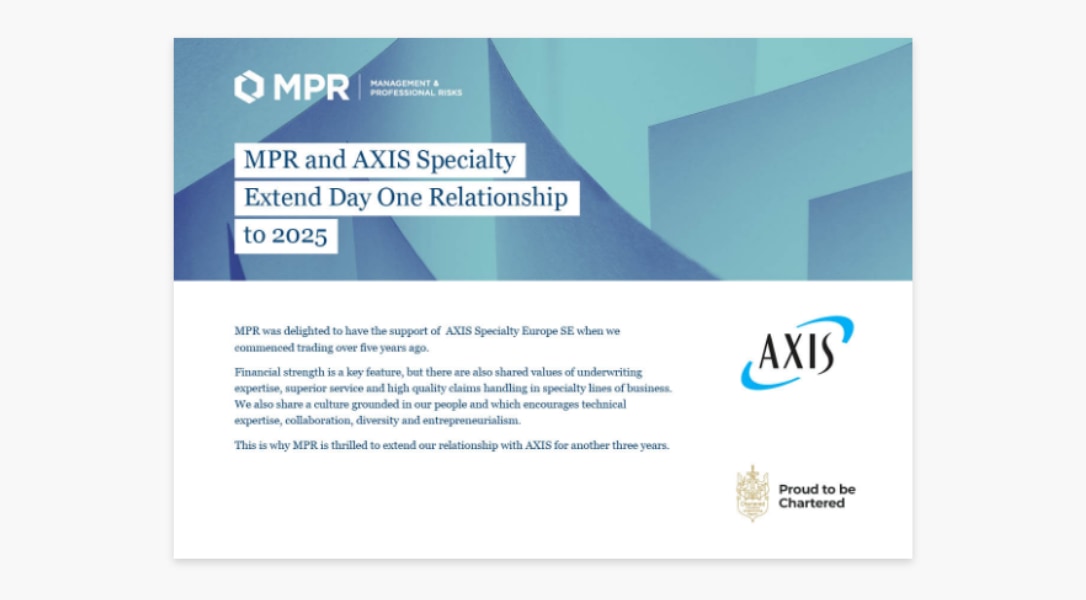

MPR is thrilled to extend our relationship with AXIS for another three years.

One of the founding ambitions of MPR was to achieve the highest professional standards.

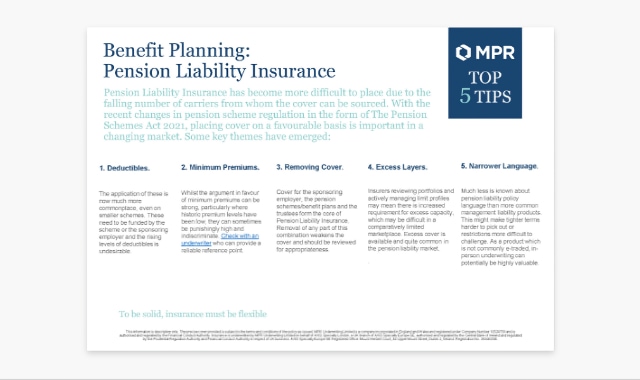

Pension Liability Insurance has become more difficult to place due to the falling number of carriers from whom the cover can be sourced.

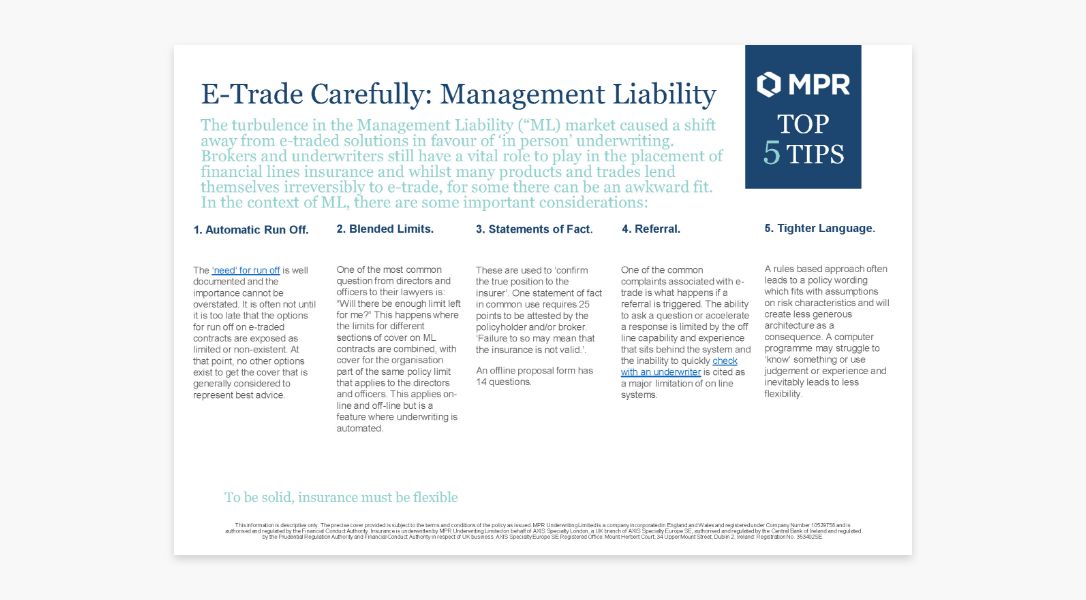

The turbulence in the Management Liability (“ML) market caused a shift away from e-traded solutions in favour of ‘in person’ underwriting.

Neil McCarthy, Managing Director at MPR Underwriting Ltd Underwriting Limited, was recently recognised in our Power Player series – D&O Insurance 2022 – Exceptional Experts.

The request to include ‘associated companies’ on a management liability policy is common. The response from underwriters is not.

The question of how to choose a Directors and Officers (“D&O”) liability policy limit is one which is frequently visited. Unhelpfully, there is no clear and unequivocal way to answer.

Governing law (or “choice of law”) and jurisdiction are quite closely linked, and are often dealt with in the same place, but they do cover 2 slightly different things.

Cyber Insurance is becoming a more challenging product to place. Frequent and severe losses, combined with a previous ‘soft’ market landscape have created profitability issues for insurers.

At a time when the PI market is just about as confusing as it has ever been, talking about Miscellaneous PI appetite can be a particularly tricky business.

We are delighted to have been ranked 5 out of 5 for the second consecutive year in the Insurance Times Broker.

A recent policy comparison highlighted ‘all employees as Insured Persons’ as the main policy feature. From the perspective of a director, I found this both curious and puzzling.

The ‘duty to defend’ is a long-standing provision in D&O policies and, in broad terms, allows the appointment of a lawyer to be the choice of the insured person(s).

The heritage of ‘Order of Payments’ or “Priority of Payments” clauses is rooted in the introduction of entity coverage to the Directors and Officers (“D&O”) policy architecture in the early 1990’s.

Risk mitigation is a key compliment to any quality insurance solution, and cyber is no different. A combination of a rise in the severity of claims and hardening market conditions has focussed attention on simple yet effective measures that insurers will look for as minimum requirements

There is little doubt that Directors & Officers (‘D&O’) Liability is a sophisticated product which contains potentially complex concepts and processes. Despite the low profile in a D&O policy features showreel, ‘allocation’ is nonetheless a key component of any contract and plays a role in all claims.

Once upon a time, deductibles were a common feature of Directors and Officers (‘D&O’) Liability policies. Typically reserved for larger or more challenging private risks, or those that were publicly listed, they faded from view as the soft market invaded every element of the contract.

Brokers were at the heart of the MPR proposition from the very start. That is why we are delighted to have secured a 5-star rating from every category of broker in the Insurance Times Broker MGA survey. *

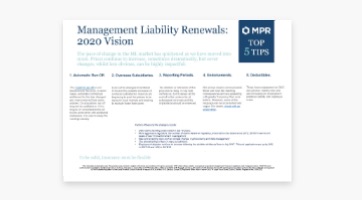

The turbulence in the Management Liability market has intensified. Price increases can sometimes draw attention away from developments in programme management, and there are recurring themes which can be as important as premium considerations.

Conversations about entity cover run off often only crystallise when the perceived requirement for cover is most urgent.

MPR feature on a podcast looking at the role of MGAs within the Insurance industry.

Latest news, market updates and product information from MPR.

The pace of change in the ML market has quickened as we have moved into 2020. Prices continue to increase, sometimes dramatically, but cover changes, whilst less obvious, can be highly impactful.

The case for solid analysis and judgemental flexibility in the underwriting process has never been more important. Here are some strategies that may help.

As Shakespeare conveyed in Hamlet, “There is nothing good or bad, only thinking makes it so.” No event or occurrence is truly good or bad, they are based on our cognitive processing and pre-suppositions.

The ubiquity with which the professional services exclusion (“PSE”) appears on D&O policies might suggest a consistent and easily communicated position. Sadly, this is far from the case.

Our ever-increasing reliance on technology to complete even the most menial of tasks in our everyday lives can provide a metaphor for businesses and how they might mitigate their exposure to these types of fraud by risk control and/or risk transfer.

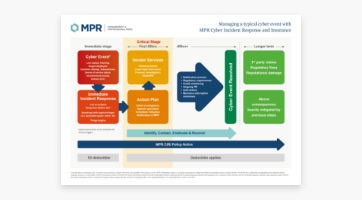

MPR’s CIRI policy specifically has an ‘Immediate Incident Response Expenses’ definition, because we want the policyholder to act without hesitation, even if they feel they may be able to handle it themselves.

Over 18 months ago, we wrote about the PI underwriters thought process in what PI underwriters care about. Since then, significant change has swept through the market.

The question of the difference between, and application of, the prior and pending litigation date (“P&P date”) and the retroactive date (“retrodate”) is a frequently visited conversation and can sometimes be difficult to decipher.

Discussions about cyber insurance policy cover and sales techniques have intensified recently, but the narrative can be high level and lacking in any real-life context.

Incident response providers have observed that a strong theme emerging, even where a cyber insurance policy in force, is poor escalation from the discovery of the cyber event to the point at which the appropriate experts are engaged.

Those of a certain vintage will recognise that ‘Difference in Conditions’ (DIC) clauses have been around for quite some time.

Anyone who has ever been involved with junior sport will know the challenges associated with keeping all those involved happy.

‘Insured capacity’ is a frequently visited subject and continues to be a central aspect in many discussions around the scope of D&O policies.

Despite a continuing increase in cyber breach events, a changing regulatory landscape (post GDPR) and a further increase in use of (and reliance on) technology, cyber insurance is still often regarded as a difficult product to sell.

With a multitude of cyber insurance products available in the UK a lot of work has been carried out on policy comparisons, but there are some product characteristics that are often overlooked or require further examination. Here are five key features and why they’re important.

In 1998, it wouldn’t have been possible to Google ‘entity cover’, because Google had only just been founded. Equally, even if you had been able to do this, there wouldn’t have been much content, given entity cover only emerged in the same year.

The case for run off on a D&O policy is well established. However, an internet search for ‘crime insurance run off’ will deliver slim pickings.

A ‘need’ is something that is necessary for an organism to live a healthy life, which, for as enthusiastic as we are about D&O insurance, is something of an ambitious claim.

The Insurance Act 2015 (“the Act”) was hailed by some as “the most profound shift in UK commercial insurance law ever”.

At the Championship play off final in 2010, Blackpool FC sold 37,000 tickets for their game against Cardiff. Seven years later, in the League Two final against Exeter, only around 5,000 tickets were sold.

The profile of litigation funding has been raised recently with the case of RBS, and there is further evidence that it is emerging as a greater threat in the event of alleged wrongdoing, whatever the nature or scale of the organisation in question.

During the many conversations around the challenges of selling cyber insurance, some common themes emerge, but these are often easily answered.

When it comes to Cyber events, we’re not talking about “if” and “when“ any more… it’s more a case of “How“… How will an organisation deal with the situation?

The technology sector continues to grow, particularly post-Brexit as the UK strives to be a leader in technological advancement. Recent reports have suggested that the UK’s digital economy is growing faster than ever.

There have many recent articles highlighting growing automation in all industries and the loss of jobs that will follow. The insurance industry is no exception and seems to be fully in the firing line.

The emergence of ‘Social Engineering’ has shattered many organisations. In this case, the hospice was duped into believing they were taking part in an on-line virus check.

Why ‘approved’ insurers are all looking to write the traditional business from a similar perspective on the same basis, with pricing and service the only real differentiators.

When considering insuring professional service firms’, the focus tends to be on the business activities, fee income and claims experience.

Cyber Crime cover from MPR Underwriting.

Many architects PI claims don’t come from typical design errors that you might expect, but from inspection duties or project management, either during the project or post completion.

A component part of many PI policies is that they provide cover for forms of defamation (most commonly libel and slander) in the course of their business activities.

The same pattern sometimes appears in business. When things go wrong, frustrated parties can act irrationally and may say things that won’t necessarily be followed up on.

When examining diamonds, the ‘Four C’s’ method is used. A diamonds value, rarity and beauty are determined by Colour, Clarity, Carat and Cut.

‘This “triumph for access to justice” will not be welcomed by all’. So declared Supreme Court judge, Lord Reed, on ruling unanimously in favour of Unison.

The duty to defend principle is an important one, and it governs how the mechanics of a claim are handled. It describes the insurer’s obligation to provide an insured with defence to claims.

This constant legislative evolution is not to suffocate organisations, but to seek to keep them honest and to protect innocent people reliant on the future of a company, such as suppliers, manufacturers or customers.

Managing a typical cyber event with MPR Cyber Incident Response and Insurance.

D&O prices are on the rise, following a decade of soft market conditions. As well as price increases, it’s important to look out for other features and potential changes at renewal.

This ‘rationalisation’ is part of a standard methodology developed by fraud investigators. It is also one aspect of the most widely accepted model for explaining why employees steal from their employers, namely the ‘fraud triangle’.

Underwriters don’t like surprises. We like the predictable and the foreseeable. Yet, every now and then, a theme emerges that wasn’t predicted or foreseen.

The Association of Certified Fraud Examiners estimates that, on average, 6% of the turnover of an organisation is lost to employee fraud.

Privacy Policy and Cookie Information

We use a small number of cookies on this website to make the website as useful as possible. None of these cookies collect any personal information. To find out more about these cookies and how to control their use, see our Read More.

Close